07 April 2026

07 April 2026

Motor Vehicle Insurance is a branch of Insurance law and a critical aspect of responsible car ownership. It aims at providing protection to the driver, the motor vehicle, passengers and other motorists whilst ensuring compliance with the law.

There are different types of motor vehicle insurance namely :

- Comprehensive Cover – Offers extensive protection, covering virtually all risks, including damage to your own vehicle and third-party liability.

- Third Party Only (TPO) – The minimum mandatory cover required by law, protecting other people and their property but not your own vehicle.

- Third Party, Fire, and Theft (TPFT) – Provides coverage for third-party liability, as well as protection against fire damage and theft of your vehicle.

- Commercial/PSV Cover – A specialized type of cover for business or public service vehicles, catering to higher risk and operational requirements.

REPUDIATION

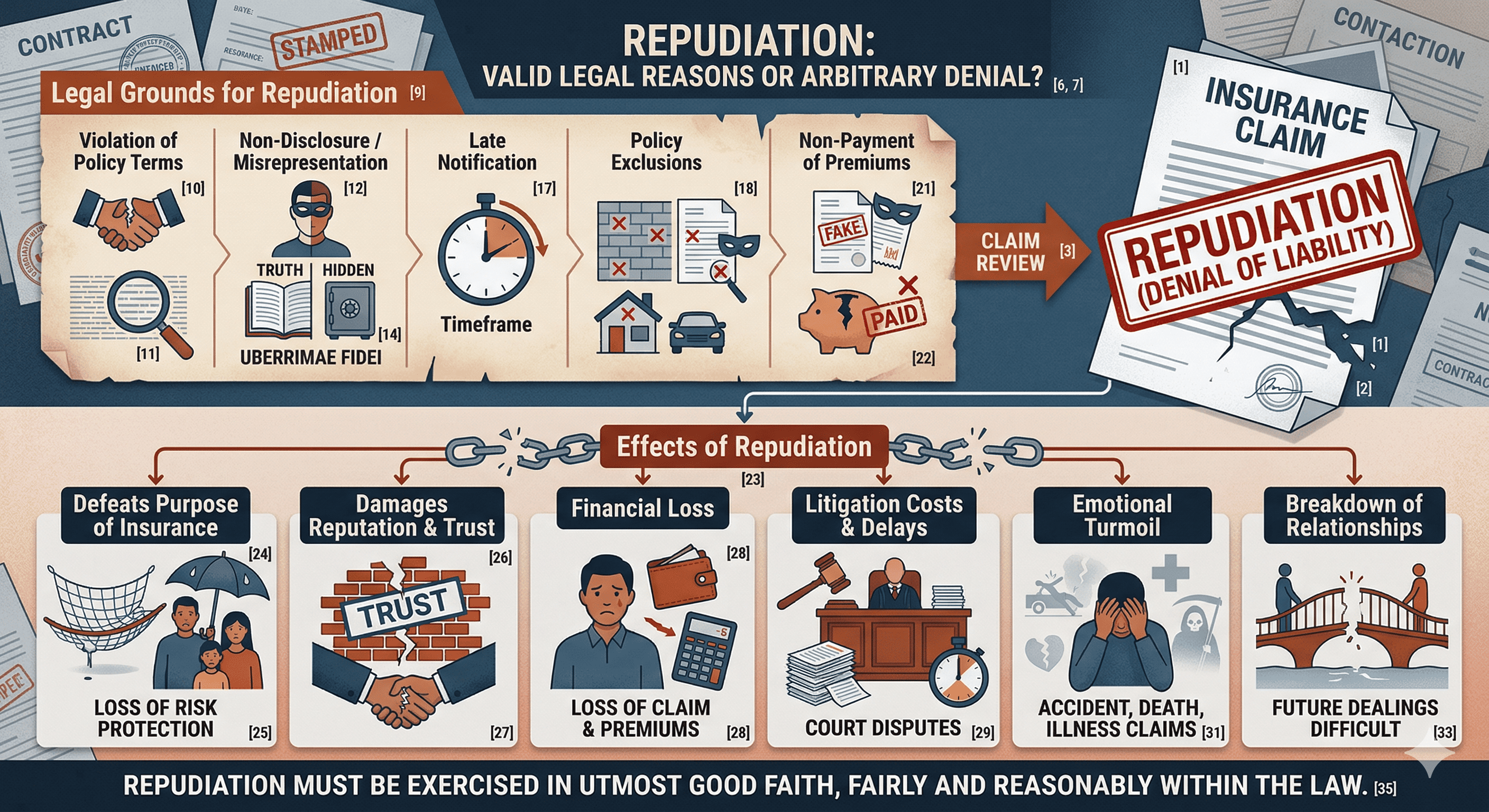

As a policyholder, you may sometimes submit a claim only to have it rejected after review and assessment by your insurer. This rejection is referred to as repudiation.

Repudiation can be incredibly frustrating, especially when you believe your claim is legitimate. Insurers may reject claims for several reasons, often related to non-disclosure, breach of policy terms, or misrepresentation.

Understanding the main grounds for repudiation can help policyholders avoid unnecessary claim disputes and protect their rights.

Grounds for Repudiation on Motor Vehicle Insurance

a. Non-Disclosure or Misrepresentation

- Failing to provide accurate information regarding the driver, car usage, or previous accidents

- violating the principle of utmost good faith.

b. Breach of Policy terms and conditions

- The vehicle was driven by unauthorized driver, driver lacked a valid driving license, driver was under the influence of alcohol or drugs

c. Breach of Usage Policy

- Using a private vehicle for commercial activities without updating the insurance, renders the policy invalid e.g. driving a private car as a tax

d. Transfer of Ownership

- Selling the vehicle and transferring the insurance certificate without notifying the insurer as the contract is between the insurer and the original owner.

e. Delayed Notification

- Failing to report the accident within the stipulated timeframe in the policy.

- In case of an accident notify your insurer within 24-72 hours – check the claim notification deadline in your policy

- If a dispute arises and you need to file a lawsuit (personal injury claim), Kenyan law under the Limitation of Actions Act allows for a period of three years from the date of the accident.

f. Fraud or fraudulent claims

- Deliberately inventing or exaggerating a loss, staging an accident, submitting forged documents or colluding with others to misrepresent facts.

g. Non-payment or lapse of premium

- If premiums are unpaid and the policy has lapsed or cover was suspended at the time of loss, claims will be rejected.

h. Wear and Tear and Mechanical breakdown

- Insurance is meant to cover unexpected and accidental losses, not losses that happen gradually or naturally over time.

i. Exclusions

- Policies list specific exclusions and claims form these exclusions are not covered

j. Unlawful acts and criminal use of the motor vehicle

- Losses arising from using the motor vehicle in illegal or criminal activities are not covered

How to Avoid Motor Vehicle Insurance Repudiation

i. Understand your policy

- who is authorized to drive

- who is covered under the policy you have applied for

- notification deadlines

- exclusions

- the terms and conditions

ii. Be truthful and honest with your Insurer when applying for a motor vehicle policy and when renewing it. Disclose all material facts like the vehicle use, drivers, past claims and any modifications on the motor vehicle.

iii. Report any and all changes promptly notify your insurer about changes in vehicle use, ownership or modifications.

iv. Act quickly after an accident

- secure safety

- take photos

- gather witness details

- notify the insurer straight away.

v. Keep good records

- retain policy documents, receipts, invoices, repair quotes and any other relevant documents

vi. Maintain the vehicle by regular servicing

vii. Never commit fraud or exaggerate facts

- dishonest claims are likely to be rejected and may lead to criminal charges.

By Mary Mwende, Lawyer – A.N. Kamau & Co. Advocates